What If The Low Is Already In?

As investors, the fear of a loss is much greater and gets more attention than the excitement of a gain. But what if we already reached the lows in October and we are now in the midst of a new bull market? James Paulsen, Chief Investment Strategist of The Leuthold Group, makes a strong case for the start of a new bull market in the following article.

What If The Low Is Already In?

By James Paulsen || November 21, 2022

There is still considerable debate about whether the bear market has yet set its low. Certainly, if the U.S. economy is headed for a deep recession, stock investors will face additional, significant downside risk. Several smart bears on Wall Street suggest the S&P 500 could decline to about 3,000—or -25% from today’s level—as analysts are forced to cut earnings estimates. However, if the economy manages to avoid recession or experiences only a modest contraction, a new bull market may already be unfolding. While, understandably, downside risk typically gets the most attention, investors should also consider what the “upside risk” could be in the coming year if the “low is already in?”

Toward that end, the accompanying charts examine the historical change in earnings and valuations during the first year of each bull market from 1990 to date.

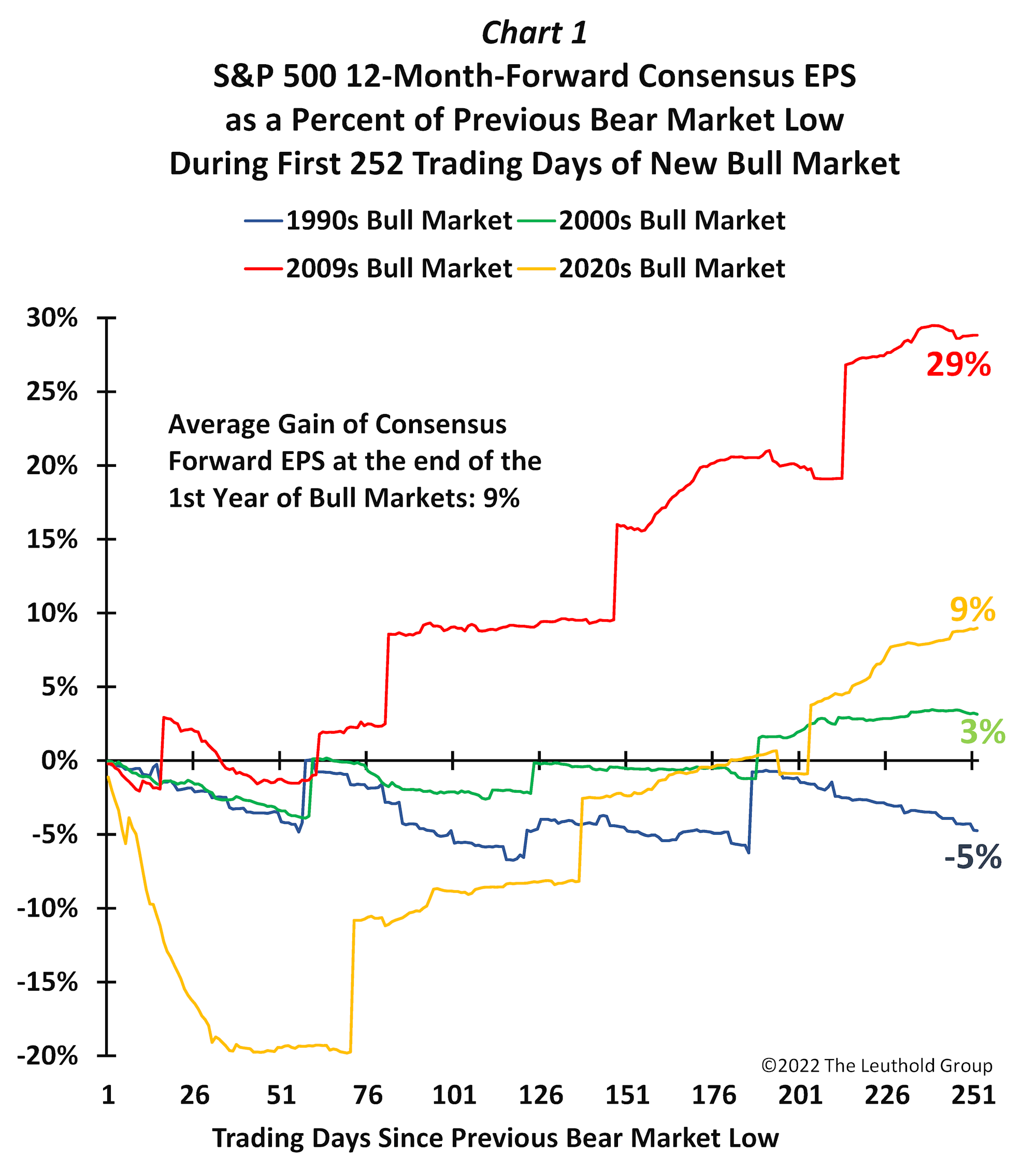

Chart 1 shows the S&P 500 change in 12-month-forward consensus EPS estimates during a bull market’s first 252 trading days, compared to those at the previous low. At the beginning of a bull market, earnings expectations usually deteriorate and, during the next twelve months, may drop beneath the levels seen at the preceding bear market bottom. In 2020, EPS were anticipated to be 20% less than the level at the S&P 500’s March low, and they stayed underwater nearly 200 trading days into the new bull market. In the 1990s’ bull, EPS forecasts were worse than at the prior bear market low for the entire first year (and were still off by 5% at the end of that twelve-month period). Similarly, in the aftermath of the dot-com collapse, twelve months into the ensuing bull market, EPS estimates were just 3% higher.

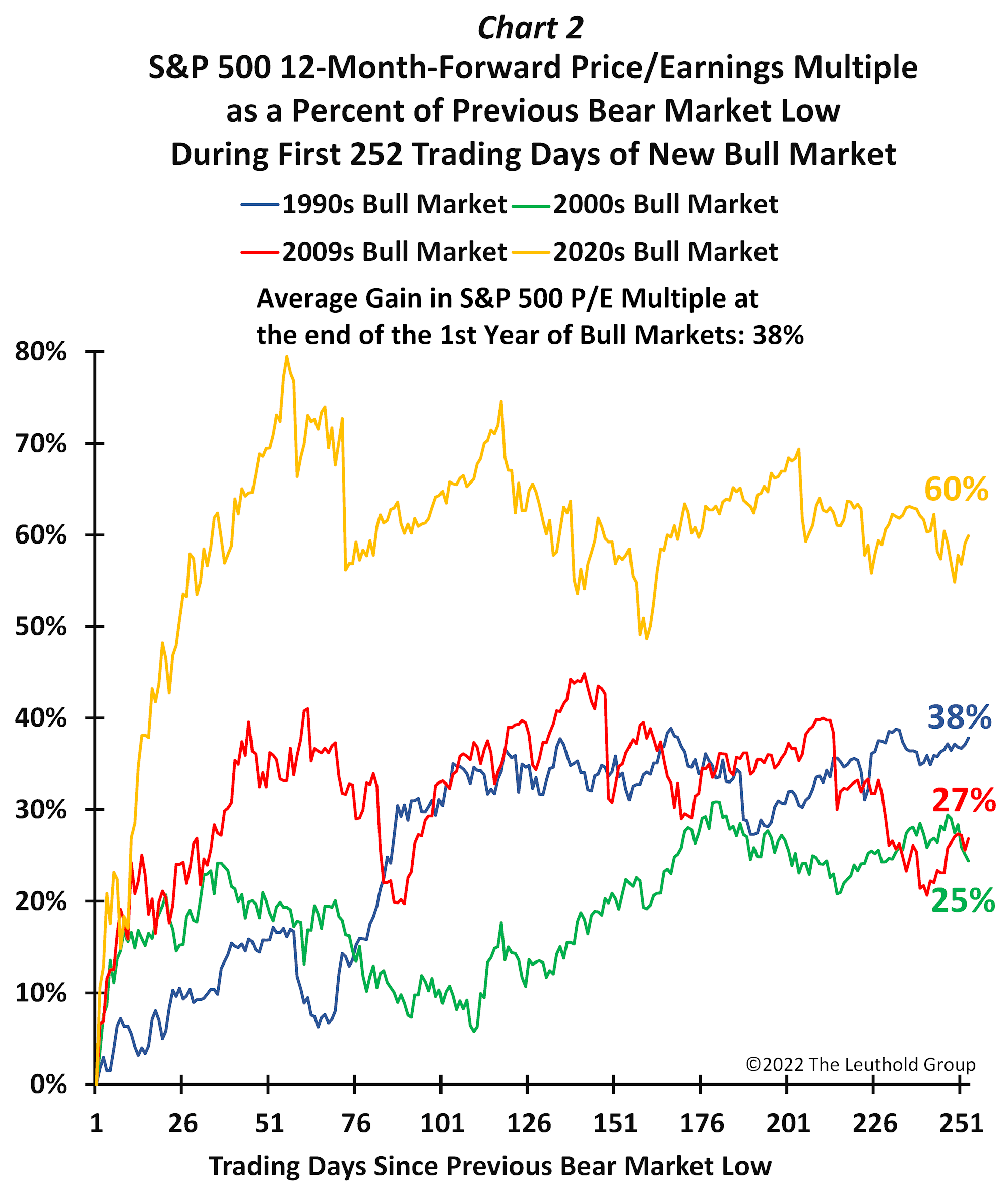

Earnings momentum is often poor in the first year of a bull market, and earnings prospects do not generally play a major role in determining the stock market’s outcome. Indeed, twelve months into the last four bull markets, EPS expectations rose by only about 9%, on average. In their infancy, bull markets are generally driven much more profoundly by improving valuations. Chart 2 illustrates how much the stock market’s forward P/E multiple increased relative to its level at the past bear market bottom: Since 1990, in the bull’s initial twelve months, valuations climbed 25%-60%, with an average gain of 38%!

Playing With Numbers?

If history is any guide, what are the prospects for stocks in the coming year, assuming a new bull market is in process? Let’s say the contemporary bear market terminated on October 14th when the S&P 500 closed at 3,583. At that point, the forward EPS estimate was about $232, and the forward P/E multiple was 15.5x.

First, assume the coming year’s P/E ratio and EPS results will equal the least productive experience of the previous four bull markets. That is, the EPS estimate sinks by 5% (like the 1990 bull), and the P/E multiple expands by just 25% (as in the early-2000 bull). EPS would fall to $220, and the P/E multiple would grow to about 19.4x—yielding an S&P 500 target of 4,270 (an 8% gain from current levels). Nothing too spectacular but not disastrous.

What if EPS and the P/E ratio expand at their respective average rates of the last four bull markets? That would be a 9% gain in EPS (to $253) and a 38% advance in the P/E multiple (to 21.4x), which would produce an S&P 500 return of +37% (5,400 level) in the coming year.

Perhaps the best approximation is to split the difference between the two scenarios: the “least constructive” of the last four bulls and the “average” outcome. That would result in an S&P 500 price of 4,835 (or +22.5%).

Nonetheless, there could be more downside at stake, particularly if a deep or protracted recession lies ahead. But investors should also consider the possibility that a bull market may be in the works by now. Who knows? Since the pandemic, economic data has been pretty messed up and difficult to document or interpret. Maybe the U.S. has already been experiencing a recession for most of 2022—rather than heading for one—and is now in the early stages of recovering.

Consumer and business confidence have certainly experienced recession-like conditions. Real GDP growth was reportedly negative in the first two quarters of this year and has been essentially flat since December. Housing has slid into a recession. The Index of Leading Economic Indicators peaked in February and has fallen for eight consecutive months. Real retail sales have risen by only 0.6% in the past year and have now contracted for six months. Is it conceivable that the stock market’s 2022 decline reflects a recession that was virtually undetected and has largely run its course?

The inflation rate has peaked, and we suspect the 10-year bond yield has also seen its high. As the pace of the economy decelerates in the coming months, recession fears are apt to intensify, forcing the Fed to begin reversing its tightening campaign. That would improve real liquidity growth and boost economic confidence. There’s a chance the bear market might not yet be finished, but one should not dismiss the risk of missing out on a new bull.

About The Author

James Paulsen Chief Investment Strategist

Jim is Chief Investment Strategist of The Leuthold Group, LLC. He is a member of the investment committee, authors market and economic commentary, and works with the Leuthold investment team.

Related Articles

Strong Earnings, Weaker Stocks: Why Hyperscaler Results Aren’t Pleasing the Market

Is AI Out Over Its Skis?

The Private Credit Mirage and Unfolding Market Stress

Resilient Data vs. Geopolitical Noise

Get In Touch

Contact our team of professionals today.

ADDRESS

3070 Saturn Street, Suite 101. Brea, CA 92821