The Age of Mistrust

The Age of Mistrust

2025 feels disorienting.

At the beginning of the year, rapidly shifting trade policies jolted markets into uncertainty. While there’s been incremental progress in negotiations, the climate remains unpredictable. Investors faced a whirlwind of threats, delays, and tentative deals, each one disrupting expectations. That lack of stability is compounded by a political environment in flux, from the firing of the Bureau of Labor Statistics commissioner over allegations of data manipulation to the public attacks on Federal Reserve Chair Jerome Powell. The tension between branches of government has led many to ask: what happens next, and what’s legal versus unprecedented?

Certainty, so valued by investors, has become a rare commodity. We’re left watching every twist and turn—not because we want to, but because the stakes are high.

Trust in traditional information channels is also under strain. Some news coverage seems designed more to provoke outrage than to inform. At the same time, the explosion of AI-driven content has blurred the line between reality and manipulation. What we read on platforms like Facebook or TikTok may not just be misleading, it could be entirely fabricated. Ironically, in an era defined by instant information, truth has never felt so elusive.

Earlier this year, markets absorbed a shock when it became clear that escalating tariffs might reignite inflation and trigger layoffs. Between February 19 and April 7, the S&P 500 fell more than 20%, entering bear market territory for the second time in three years. Analysts downgraded earnings expectations, and CEOs began to temper their financial outlooks. Consumer confidence dropped sharply. A recession felt not just possible, but probable.

And yet, by late spring, the market had recovered nearly all those losses. The S&P 500’s rebound was swift and strong. So, what happened?

There’s an old market phrase: “climbing a wall of worry.” It means rallies often begin when conditions still look bleak—because investors start to anticipate a brighter horizon, even before it’s fully visible. That’s exactly what we’ve seen.

The most extreme tariff scenarios didn’t materialize. While trade disputes are far from resolved, the actual tariff levels now look more manageable, closer to 15%, not the originally threatened 35%. Investors began to interpret some of the earlier bluster as strategic positioning rather than policy certainties.

And while the economy has cooled somewhat, it hasn’t stopped. Inflation is modestly higher due to tariffs, and hiring has slowed in sectors like construction, retail, and autos. But layoffs remain low. Consumer spending is stable. The same survey of Wall Street economists who predicted growth as low as 1.0% this year revised their estimates upward to 1.7%. In other words, recession fears are receding.

Crucially, second-quarter corporate earnings beat expectations. Nearly all companies in the S&P 500 have reported, and results show year‑over‑year revenue growth near 6% with earnings‑per‑share up around 11%. Businesses are adapting, reworking supply chains, managing costs more efficiently, and embracing new technology. And the AI boom isn’t just hype. It’s already showing up in the numbers, with tech companies continuing to invest and grow despite the political noise.

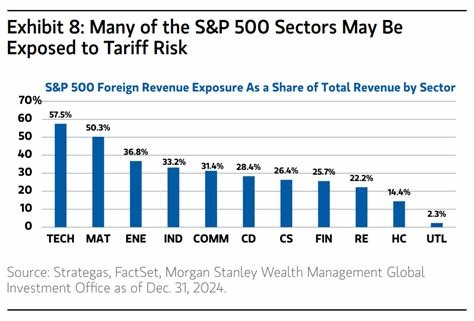

Here’s where things get even more interesting. Different sectors are experiencing very different levels of impact from trade policy. Some, like technology and materials, face higher exposure to tariffs due to global supply chains and foreign revenue dependencies. Others, like utilities or domestic consumer services, are more insulated.

Understanding these sector-level dynamics helps explain why the broader market can rally even while some industries feel pain. Investors are becoming more selective, looking past the headlines and focusing on areas of real strength.

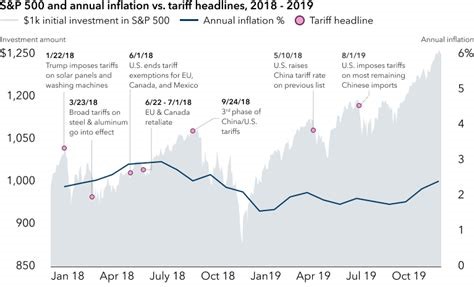

Historically, this isn’t the first time we’ve faced this. A similar tariff scare during the 2018–2019 period produced market volatility and inflation worries, but the long-term impact was less damaging than feared. Back then, markets adjusted as businesses recalibrated and consumers adapted.

Today’s situation echoes that pattern. Policy headlines remain loud, but underlying fundamentals are proving more resilient.

Professional investors have taken note. Analysts like Mike Wilson at Morgan Stanley now believe a new bull market is forming. Others, like Blackrock’s Rick Rieder, have called this the best investment backdrop in decades. These views may appear optimistic, but they reflect a shift in mindset: from defensive caution to cautiously optimistic engagement.

Of course, uncertainty hasn’t vanished. Trade tensions could still flare. The job market could cool more than expected. Inflation might tick higher. But investors no longer expect worst‑case scenarios as the default outcome. That’s a meaningful change.

At this stage, the long-term positives, corporate adaptability, AI-driven productivity, and modest economic growth, are beginning to outweigh the political and policy-related negatives. The path ahead may still be uneven, but the footing is firmer than it was just a few months ago.

Related Articles

Strong Earnings, Weaker Stocks: Why Hyperscaler Results Aren’t Pleasing the Market

Is AI Out Over Its Skis?

The Private Credit Mirage and Unfolding Market Stress

Resilient Data vs. Geopolitical Noise

Get In Touch

Contact our team of professionals today.

ADDRESS

3070 Saturn Street, Suite 101. Brea, CA 92821